ChinaKnowledge.de -

An Encyclopaedia on Chinese History, Literature and Art

Piaohao 票號, also called piaozhuang 票莊, huihao 匯號 or huiduizhuang 匯兌莊, were private banks, in the late Qing period 清 (1644-1911).

In the late Ming period 明 (1368-1644), letters of exchange or money orders (huipiao 匯票 or 會票) were already widely used as a means of remittance (huidui 匯兌, bodui 撥兌). From the late 17th century on, the growing interregional trade required a more elaborated system of credit, exchange and remittance which caused the spread of piaohao banks. Most important was the development of local banks in the districts of Pingyao 平遙, Qixian 祁縣 and Taigu 太谷, Shanxi.

The most important of the three banking groups (sanbang 三幫) in that region were the Rishengchang Bank 日升昌票莊 (founded in 1821), which had emerged from a retailer in dyestuffs, the Five United Weizi Banks (Weizi wulian hao 蔚字五聯號, with Weitaihou 蔚泰厚, Weifenghou 蔚豐厚, Weishengzhang 蔚盛長, Xintaihou 新泰厚, and Tianchengheng 天成亨, formerly operating in the silk business) from Pingyao, the Heshengyuan Bank 合盛元號 (based on the tea trade) from Qixian, or the Zhichengxin Bank 志誠信號 (also former silk traders) from Taigu. The history of these houses shows that it were merchant families who began engaging in the monetary business, often without giving up their original trade. Because the credit business was overwhelmingly controlled by merchant-banks from Shanxi, they were also known as Shanxi piaohao 山西票號, or the Shansi Banks, as called by foreigners. Shanxi merchants were so much related to the financial business that they were called kedui 克兌 "changers" or keqian 克錢 "moneylenders".

|

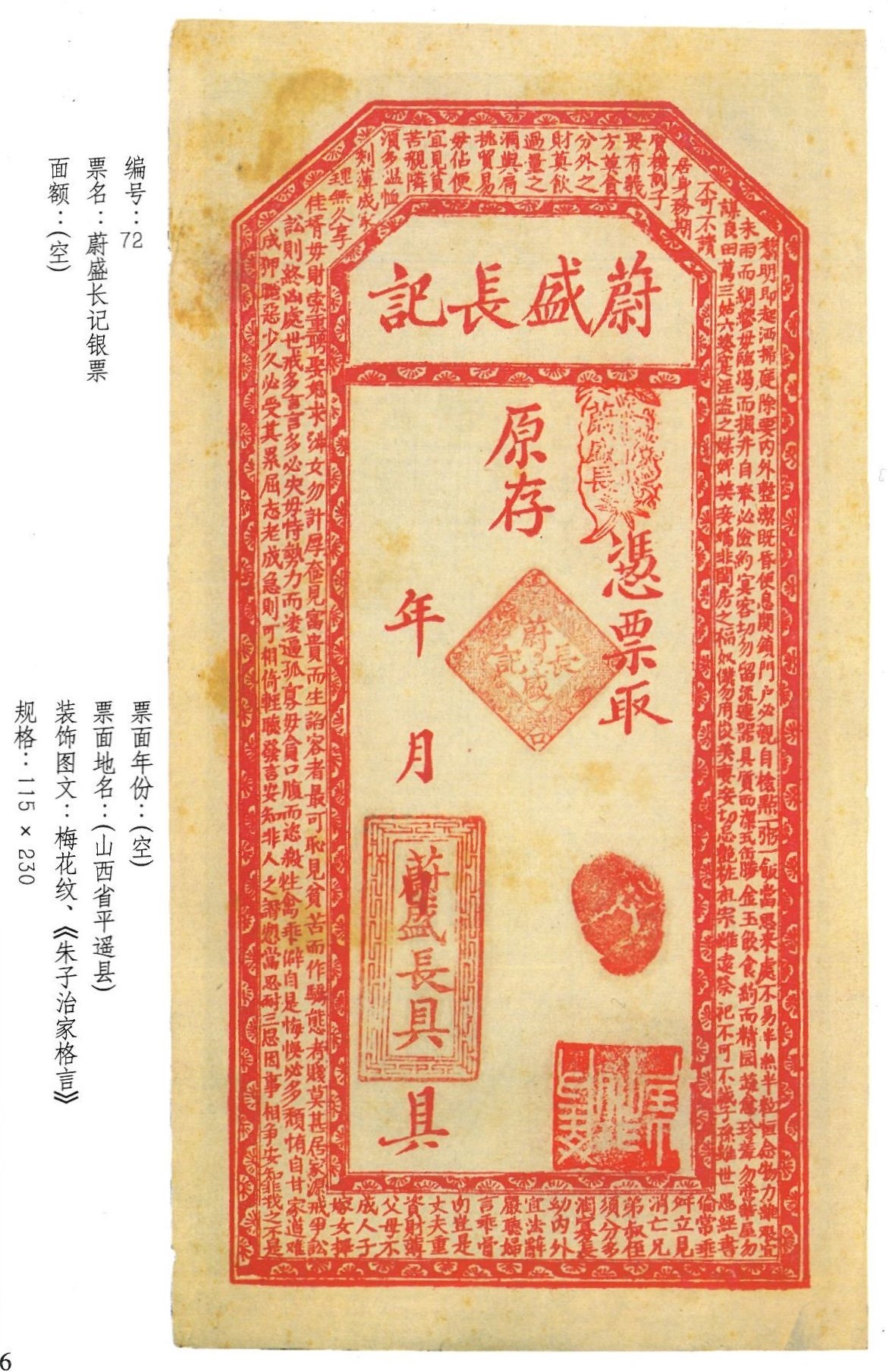

Blank form of a remittance note of the Weishengzhang Bank 蔚盛長, size 115×230mm. The outer band is decorated with sentences from the primer Zhuzi zhijia geyan 朱子治家格言. Click to enlarge (opens in new tablet). Source: Liu & Wang 2001: 186. |

Most of the Shanxi Banks were founded on joint investment (hehuo 合伙). Only a minor number had a single investor. The height of the capital stock ranged from about 20,000 liang/tael (see silver currency) to 500,000 tael, yet because most banks reserved an amount of capital protected (huben 護本, beiben 倍本), the operative capital was much less. The reserves were kept in the head office (zonghao 總號), where the household of the bank owner was registrated. The Shanxi Banks had branches (fenhao 分號) in every larger city. The remittance of money was thus easily possible between the head and the branch offices. They had branches throughout the country, but the core area was north China.

In their heydays there were 32 independent banks, with more than 400 branch offices in the whole of China, and some abroad (Tōkyō, Kobe, Yokohama, Incheon, Moscow, Kolkata or Singapore). Every three or four years, an account (jiezhang 結賬) was provided to the shareholders, and dividends distributed. The common form of "shares" was of course money (yingu 銀股), but some shareholders guaranteed with their office and the expectable salary. This was called "person-based share" (rengu 人股 or dingshengu 頂身股). Some Shanxi Banks issued their own paper bills (duitie 兌帖, qitie 期帖, qiantie 錢帖, yinpiao 銀票) with different functions (many of them representing letters of exchange), thus making good for the missing of a kind of paper currency in the monetary system of the Qing period, and for the failure of the paper bills issued during the Xianfeng reign-period 咸豐 (1851-1861).

The Shanxi Banks operated in daily business mainly with monetary remittances (huidui). The remittance fee (huifei 匯費, huishui 匯水) depended on the distance, the urgency, and the quality of the silver paid to the remitting bank. The fee to be paid by the remitter was also called liqian 力錢. It was either two tael (shuangli 雙力) per 100 tael of money remitted, or one tael (danli 單力). Local differences in the value of silver ingots could be used for profits by arbitrage business (yaping case 壓平擦色). Another important part of the business was the assaying of silver and the production of silver ingots (wenyin 紋銀). The most important customers of the Shanxi Banks were merchants in interregional trade (bangji maoyi 埠際貿易), yet from the time of the Taiping Rebellion 太平 on the Shanxi Banks took over for the government the remittance of funds (huijie 匯解) to other provinces (xiekuan 協款, xiexiang 協餉) or advanced the payment for troops (xiangyin 餉銀, junxiang 軍餉) or funds for the infrastructure of the local governments (xinjin 薪金).

Apart from that, they also offered the deposit of funds (cunkuan 存款) and credits (fangkuan 放款) to the local government (then called guankuan 官款), state officials, or private persons. The reputation of the Shanxi Banks was very high, and a huge number of persons confided them their money, in spite of the low interest rate (in contrast to the very high interest rate on credits). Credits were also given to smaller banks in southeast China (see qianzhuang 錢莊), pawnshops (diandang 典當) and the great merchant houses. Last but not least, the Shanxi Banks took over the purchase (juan guan 捐官) of brevet titles (xian 銜, see contribution system) or advanced money for the purchase of a vacancy (mou que 謀缺).

The Shanxi Banks profited enormously from the "great contribution campaign" (dajuan 大捐) of the Qing government carried out the finance the war against the Taiping rebels, with an amount of at least 2.6 million tael advanced for the purchase of offices. The Shanxi Banks were also crucial in the modernization attempts carried out in the late 19th century. Financial investments for factories and railways, for instance, were to a large extent only possible with the credit of the Shanxi Banks. The Shanxi Banks in Shanghai offered the subscription (rengou 認購) of bonds like the Zhaoxin share (Zhaoxin gupiao 昭信股票 from 1898) or that issued to finance the Boxer Indemnity (gengzi beikuan 庚子賠款). They also issued shares themselves which did, as that of the Dadetong Bank 大德通票號, yield enormous profits. Valued at 850 tael in 1889, their shares stood at 3,150 tael in 1896, 4,024 tael in 1990, and at 17,000 tael in 1908.

In the second half of the 19th century, a group of southern banks (nanbang piaohao 南幫票號, usually called yinhao 銀號) was created by local merchants in the province of Zhejiang. These were, for instance, the Yuanfengrun Bank 源豐潤票號 or the Yishanyuan Bank 義善源票號. During that time the qianzhuang banks became more important, as they had close connections to the foreign banks that began investing in China, particularly in Shanghai. Yet the financial power of the Shanxi Banks still allowed them a superior position, as the smaller qianzhuang banks often led money from them. In 1875, 24 Shanxi Banks founded the common office, the Shanghai Banking Association (Shanghai huiye gongsuo 上海匯業公所). The Shanxi Banks were, furthermore, backed by the government, the officialdom, wealthy merchants and landowners. Contact between the Shanxi Banks and foreign banks or merchants was rather indirect, and passed only through the mediation of the local qianzhuang banks.

Around 1900 the heyday of the Shanxi Banks was over, even if they still had operating capital of more than 200 million tael. The qianzhuang banks had gradually taken over the Shanxi Banks' fields of business. In addition to that, each province founded a government bank (guanyin qianhao 官銀錢號), and the central government, too, created national banks (Commercial Bank, tongshang yinhang 通商銀行, Bank of Communications, jiaotong yinhang 交通銀行, Bank of the Ministry of Revenue, hubu yinhang 戶部銀行, later Da-Qing yinhang 大清銀行).

After 1912 practically all Shanxi Banks closed or transformed into more modern types of banks.